Date uploaded: 2021-10-14 14:52:14

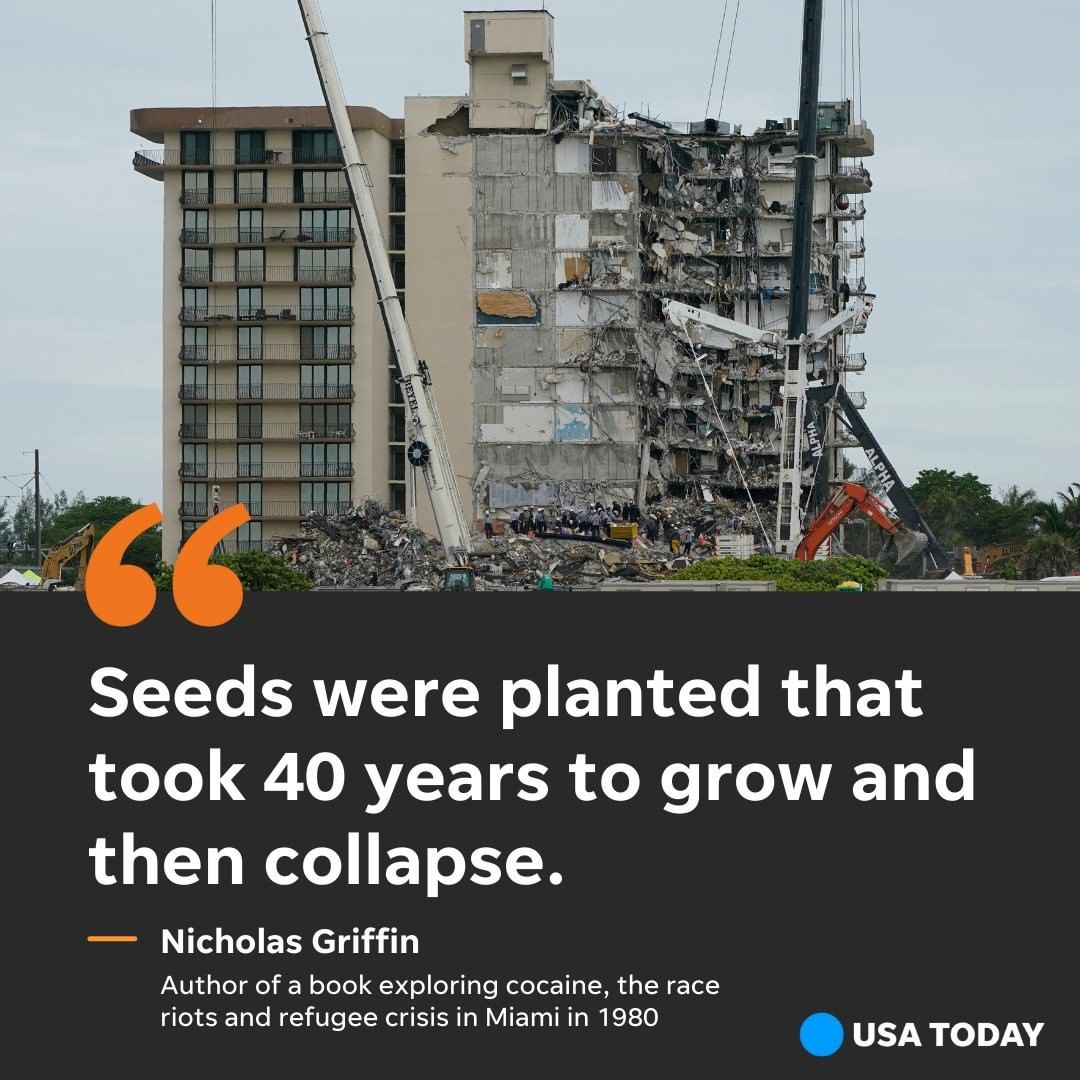

Whem Champlain Towers South ascended from the beachfront 40 years ago in the quaint Miami suburb of Surfside, the new condominium gleamed with promise.

It was the first swanky high-rise condo in the tiny town, and it solidified the neighborhood as a gathering place for the rich and famous like Frank Sinatra, who hung out down the road from where the high-rise stood. For its residents – from millionaire cocaine smugglers to family vacationers – it was all about landing their little slice of paradise.

But even before developers sold off the 136 condominiums to their first owners, the construction had been botched and the building had been set on a course to rot from the foundation up, a USA TODAY investigation shows.

The reporting reveals for the first time that early condo sales exhibit tell-tale signs of a money laundering scheme. Experts say cutting corners on construction often accompanied money laundering.

At Champlain South, engineers have noted an incorrectly designed pool deck and improperly constructed support columns. Money laundering also might have meant that some early buyers weren’t living in the condo building or concerned with its long-term maintenance.

Even when engineers finally alerted residents to design flaws that were causing chronic water intrusion and growing damage to concrete, the arguments and delays over needed repairs did not focus on safety, but rather about the cost and inconvenience of fixing the problems.

USA TODAY set out to compile a complete accounting of the forces at work on the building that collapsed on June 24, killing 98 people. The investigation reveals the rise and fall of Champlain’s fortunes, from one of the most expensive in the region to a tarnished bargain.